What Is a Loan Origination System? A Plain-English Guide for New Brokers

Most new loan officers hear "LOS" in their first week and never get a straight answer about what it actually does. This guide walks through what a loan origination system handles (document tracking, compliance checks, automated disclosures, underwriting integration) versus what it doesn't - lead follow-up, Realtor relationship tracking, and pipeline visibility before a file even opens. It covers the six stages of mortgage loan origination from application to close, what to look for in loan processing software, and the most common tech stack mistakes brokers make in their first year.

The core takeaway: a LOS manages active loan files, a mortgage CRM manages everything before and after. Brokers who set up both early, rather than waiting until volume forces the issue , close more loans with fewer leads slipping through the cracks.

Nobody explains the tech stack to new brokers. You get licensed, you get your first few leads, and then someone mentions "the LOS" and you nod like you know what they mean. Most people don't ask. They google it later and land on a 4,000-word article clearly written for enterprise lenders with six-figure software budgets.

This guide isn't that. It's for someone who just got their license, has real borrowers coming in, and wants to understand what a loan origination system actually does and whether you need one right now.

What "Loan Origination" Actually Means

Before the software, the term. Mortgage loan origination is the full process of taking a borrower from "I want a mortgage" to "here are your keys." That covers the application, document collection, credit check, underwriting review, compliance checks, and final approval. The whole chain.

An origination fee (typically 0.5%–1% of the loan amount) is what lenders or brokers charge for this work. When people talk about "how long origination takes," they usually mean 30–45 days from application to clos, though that depends heavily on how fast the borrower gets you their docs.

A loan origination system (LOS) is the software that manages all of that. Think of it as the pipeline manager for your loan files. Every stage of the process, every document, every compliance check lives in there.

What a LOS Does (And Doesn't Do)

Loan origination software handles the operational side of the mortgage process:

- Collecting and organizing the borrower's 1003 application

- Tracking which documents are in, which are missing, and who needs to follow up

- Running automated compliance checks; TILA, RESPA, HMDA, the alphabet soup you'll memorize fast

- Generating loan disclosures and estimates within legally required timeframes

- Moving files through stages: application → processing → underwriting → approval → closing

- Logging audit trails so you can prove you did things correctly if regulators ever ask

What it generally doesn't do: manage your relationships with borrowers before they become active files, run marketing campaigns, track referral partners, or give you any visibility into leads going cold. That's where mortgage CRM software comes in, and yes, they're different tools, even though vendors sometimes blur the line.

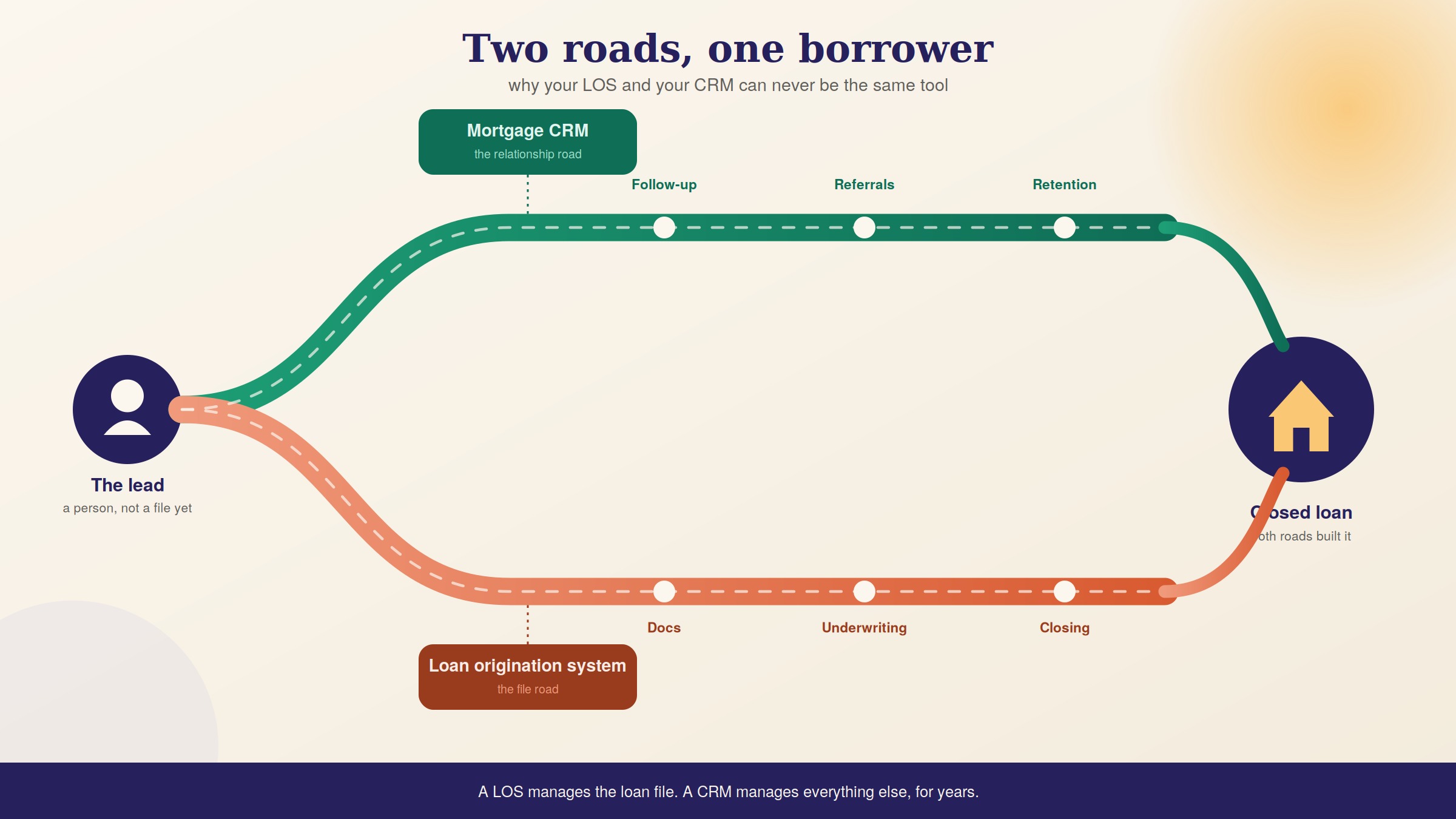

LOS vs. Mortgage CRM: The Distinction New Brokers Always Confuse

This trips up almost every new broker in the first six months.

A LOS is built for active loans. Once a borrower is in the pipeline, that's where the file lives, gets processed, and moves to close.

A mortgage CRM is built for relationships before, during, and after the loan. It handles mortgage lead management, automates follow-ups, tracks Realtor referral relationships, and keeps you in front of past clients who might refinance or send someone your way. A loan officer CRM tells you a lead went cold two weeks ago. The LOS has no idea that person exists.

The failure mode is using your LOS as a CRM. Your LOS doesn't care that a lead stopped responding three weeks ago. It doesn't send a birthday text to a borrower you closed two years back. It doesn't tell you which Realtor sent you the most purchase deals last quarter.

Brokers who try to use one tool for both usually end up doing neither well. That's how deals fall through, not because of rates, but because of follow-up gaps.

If you want to understand why follow-up is where most brokers lose revenue, the Moserbus blog covers it in detail: The #1 Reason Loan Officers Lose Deals (And How to Fix It in 2026).

If you'd rather see how a mortgage-specific CRM handles this in practice, book a 15-minute demo and we'll walk through it with a live account.

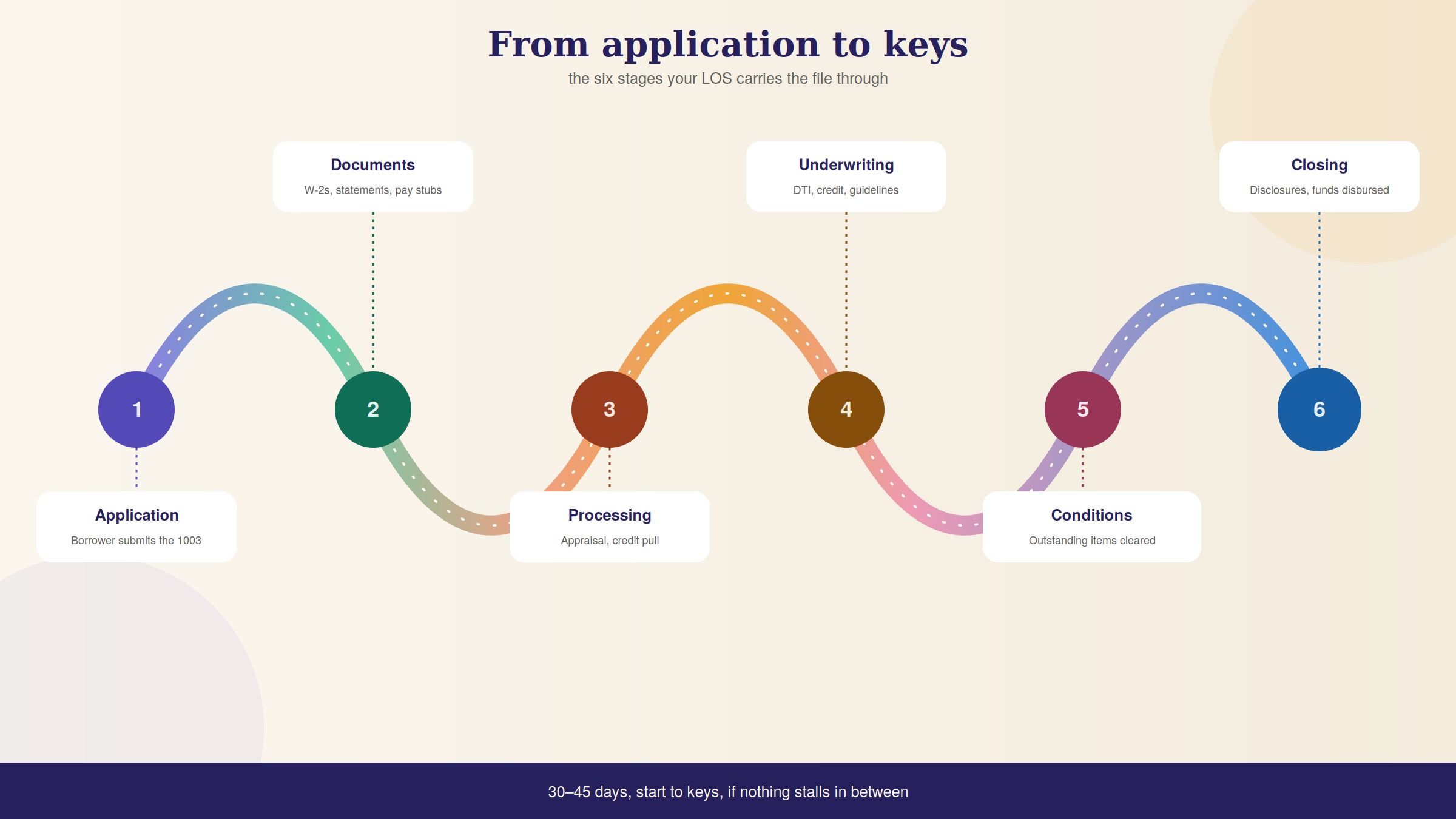

The Stages of the Loan Origination Process

Understanding what a LOS manages means understanding what mortgage loan origination actually looks like stage by stage.

Stage 1 : Application. The borrower fills out the 1003 Uniform Residential Loan Application. A good digital mortgage platform lets them do this online from any device. You collect income, employment, assets, and the property details. The mortgage point of sale (POS) system usually handles this front-end piece and feeds directly into the LOS.

Stage 2 : Document Collection. This is where most deals slow down. W-2s, tax returns, bank statements, pay stubs. The LOS tracks what's in and what's missing. Better systems auto-send reminder messages to borrowers who haven't uploaded yet, which is one of the first places mortgage automation saves you real time.

Stage 3 : Processing. A processor verifies what the borrower submitted, orders the appraisal, and pulls the credit report. The LOS keeps everything in one place so nothing falls between someone's inbox and yours.

Stage 4 : Underwriting. The underwriter reviews the full file for risk - debt-to-income ratios, credit history, property value, and whether the loan fits the guidelines for the product (conventional, FHA, VA, USDA each have their own rules). The automated underwriting system (AUS) - Desktop Underwriter for Fannie, Loan Product Advisor for Freddie - runs the initial check. The LOS integrates with both and flags compliance issues before the file reaches a human underwriter.

Stage 5 : Approval and Conditions. Most loans don't come back clean. They come back with conditions: "Provide a letter explaining that employment gap" or "We need an updated bank statement." Mortgage workflow automation at this stage tracks every outstanding condition and who's responsible for clearing it. The difference between a 30-day and a 50-day close often comes down to how well this is managed.

Stage 6 : Closing. The file gets cleared to close. Final disclosures go out, the closing date gets confirmed, funds are disbursed. The LOS documents the entire trail.

If any stage gets stuck, the LOS is where you go to figure out why.

What to Look for in Loan Processing Software

Not all LOS platforms are built the same. Here's what actually matters for a broker rather than a large retail lender or bank:

Cloud-based access. You're probably not sitting at the same desk every day. A system that only works on one installed machine is a liability. Cloud-based means you can work a file from your laptop, your home office, or wherever you happen to be.

Wholesale lender integrations. As a broker, you're submitting files to multiple wholesale lenders. Good loan processing software connects directly to those lenders so you're not re-entering data manually. Every duplicate entry is a chance for an error.

Automated disclosure generation. Loan Estimates and Closing Disclosures have strict timing windows. A 3-business-day rule isn't flexible. Your LOS should handle this automatically, not leave it to a calendar reminder.

Mortgage compliance software built in. TRID, HMDA, RESPA, these aren't optional and they don't care about your volume. A system that flags issues before you submit to underwriting saves you from expensive corrections, or worse.

LOS-CRM integration. If your LOS and your mortgage CRM software don't talk to each other, you're entering the same borrower data in two places. Make sure the tools connect natively or through a platform like Zapier.

Scalability and pricing. Enterprise LOS software can run thousands of dollars per month. For independent brokers, cloud-native options like LendingPad or Calyx Point have much lower entry points some with free tiers. Don't overbuy for where you are now.

Mortgage Pipeline Management: What You Actually Need Visibility Into

Mortgage pipeline management is about knowing the status of every active loan at a glance- what's in underwriting, what's waiting on the borrower, what's stuck, and what's closing this week.

A LOS gives you that visibility once a file is open. But pipeline in the broader sense; who's a warm lead, who's been pre-approved, who went quiet two weeks ago, who needs a rate check, that's the CRM's job.

The brokers who close the most loans are the ones who have visibility at every stage, not just once the paperwork starts. Mortgage automation handles the work of moving between those stages without someone manually chasing every person involved.

Most general-purpose CRMs weren't built for this. They don't understand milestone-based workflows, RESPA compliance timelines, or what a "clear to close" actually means. Using HubSpot or Salesforce for mortgage pipeline management is like using Excel for payroll technically possible, deeply painful.

That's exactly what the Moserbus team breaks down here: Why Traditional CRMs Fail Loan Officers.

Where a Mortgage CRM Fits Alongside Your LOS

Here's how most successful brokers think about the tech stack:

The LOS handles the loan file. The CRM handles everything else.

From the first touchpoint with a lead to the referral they send three years after close, the CRM is doing the work. Automated follow-up sequences, Realtor relationship management, mortgage lead management across your full prospect list, marketing campaigns; none of that lives in a LOS.

The problem is that most brokers delay adding a CRM until they're "big enough." The brokers who grow fastest set up their relationship management system early, before leads start slipping through the cracks.

That's the problem Moserbus was built to solve; mortgage CRM software built specifically for loan officers, with AI-powered follow-up, automated marketing, and loan milestone tracking from day one. No adapting a generic tool to your workflow. See what Moserbus does differently →

Common Mistakes New Brokers Make With Their Tech Stack

Using email and spreadsheets as loan processing software. Works until it doesn't. Ten active files and you'll miss something. That something is usually a disclosure deadline.

Thinking the LOS replaces client communication. It doesn't. Borrowers going quiet mid-process is one of the top reasons deals die. Your LOS won't send a text reminding someone to upload their bank statement, your mortgage CRM will.

Picking enterprise software because it looks credible. A 200-page manual, a six-month onboarding process, and an annual contract aren't signs of quality. They're signs of software built for a company ten times your size.

Ignoring mortgage lead management until it's too late. The leads you don't follow up with go to whoever does. Every week without a system is a week of compounding lead loss.

Does Every New Broker Need a LOS Right Away?

Honestly, it depends on your volume and your setup.

If you're working through a broker shop or a net branch, they probably have a LOS already. You'll use theirs. In that case, your priority is the CRM side; managing leads, referral partners, and client relationships is where you'll actually differentiate yourself.

If you're setting up your own operation, a LOS becomes necessary faster than you'd expect. Even at low volume, mortgage compliance software requirements don't scale with your workload. Miss a disclosure deadline on loan two and you'll wish you had the system in place on loan one.

The order most solo brokers find works: get a loan officer CRM running early, ideally before you have leads, not after you're drowning in them and add the LOS either through your broker network or as a standalone once volume justifies it.

Quick Reference: LOS vs. Mortgage CRM

| What you need to do | Tool |

|---|---|

| Track loan files from application to close | Loan Origination System (LOS) |

| Mortgage lead management and follow-up | Mortgage CRM |

| Automate disclosure generation | LOS |

| Send follow-up emails and texts | Mortgage CRM |

| Compliance and audit trail | LOS |

| Realtor and referral partner tracking | Mortgage CRM |

| Document collection and status | LOS |

| Mortgage pipeline management across leads | Mortgage CRM |

| Automated underwriting system integration | LOS |

| Post-close client retention campaigns | Mortgage CRM |

The Bottom Line

A loan origination system is the infrastructure that keeps your loan files compliant and moving. Without it, you're managing disclosure timelines manually and hoping nothing slips. With it, you have a structured process that scales.

But a LOS alone won't grow your business. Relationships, referrals, repeat clients; that's mortgage CRM software territory. The brokers who build both sides of the stack early are the ones who close more without burning out trying to keep track of everything in their heads.

If you're still figuring out what software you actually need to run a mortgage business, the Moserbus blog has a lot more where this came from.

Book a demo; takes 15 minutes and you'll see exactly how the pipeline, follow-up, and mortgage lead management work in practice. Or sign up free if you'd rather explore on your own.

Frequently Asked Questions

What is a loan origination system (LOS) in simple terms?

A loan origination system is software that manages a mortgage from the initial borrower application through to closing. It tracks documents, automates compliance checks, generates disclosures, and keeps the loan file moving through each processing and underwriting stage.

What is the difference between loan origination software and mortgage CRM software?

Loan origination software manages the transactional, compliance-heavy side of active loan files. Mortgage CRM software manages borrower relationships, mortgage lead management, Realtor partner tracking, and automated follow-up before, during, and after the loan closes. You typically need both.

What should new mortgage brokers look for in loan processing software?

Cloud access, wholesale lender integrations, automated disclosure generation, built-in mortgage compliance software, and an affordable pricing model. Don't buy enterprise-scale software if you're doing five loans a month.

What is a mortgage point of sale (POS) system and how does it connect to a LOS?

The POS is the borrower-facing application portal where borrowers start their application online. The LOS is the back-end where the file gets processed, underwritten, and closed. Most modern digital mortgage platforms integrate the two, or offer both in one.

What does mortgage workflow automation actually handle?

In a properly set-up system: document reminder messages to borrowers, condition status notifications, milestone alerts to Realtors, compliance deadline tracking, and follow-up sequences for cold leads. Done right, you're not manually chasing anyone for updates.

How long does the mortgage loan origination process take?

Typically 30–45 days from application to close, though borrower responsiveness is the biggest variable. A well-set-up LOS with mortgage automation handling document requests and compliance tracking can shorten this meaningfully.

What does a loan origination fee cover?

Usually 0.5%–1% of the loan amount, covering the cost of processing the application, underwriting review, and preparing the loan. It's separate from third-party costs like the appraisal, title, and escrow fees.

Stop managing mortgage leads in a spreadsheet. Try Moserbus free → or book a quick demo to see it live.