Salesforce Implementation for Mortgage Lenders: The Complete 2026 Guide

Every few months, a mortgage broker or a mid-size lending shop asks the same question: should we just move everything to Salesforce? It sounds like the safe, grown-up answer. Every enterprise uses it. Every consultant recommends it. And on paper, Salesforce CRM software, whether that's Sales Cloud, Service Cloud, or Financial Services Cloud, looks built for exactly this kind of work: pipelines, referral partners, compliance trails, the works.

Then someone gets a quote for the implementation, and the conversation changes.

This guide walks through what a Salesforce implementation actually involves for a mortgage lender in 2026, what it costs beyond the sticker price, where it tends to fall apart for loan officers specifically, and what to check before you commit a year of budget to it.

What Salesforce Implementation Actually Means for a Mortgage Shop

"Salesforce implementation" isn't a single product you switch on. It's a project. You're buying a license (usually Sales Cloud or, for financial institutions, Salesforce Financial Services Cloud), and then you're paying someone, either an in-house admin or an outside implementation partner, to configure it for how your business actually works.

For a mortgage lender, that configuration is not small. It means building out custom objects for loan files, borrower stages, referral partner tracking, and compliance logging, because none of that ships ready-to-use out of the box. Salesforce is a platform, not a mortgage CRM. Jungo exists specifically because Salesforce needed a mortgage layer built on top of it before it was usable for loan officers day to day. That layer took years to build and still requires its own setup process on top of the underlying Salesforce implementation.

So when a lender says "we're implementing Salesforce," what they usually mean is: we're implementing Salesforce, plus a mortgage-specific app on top of it, plus custom fields, plus integrations to their LOS, plus data migration from whatever loan origination software or spreadsheet system they were using before.

The Real Salesforce Cost and Timeline Nobody Mentions Upfront

Licensing is the smallest line item. A Salesforce Financial Services Cloud seat runs into real money per user per month before you've configured a single field. The bigger spend is the implementation itself.

Hiring a Salesforce implementation partner for a financial services build typically runs from the low tens of thousands into six figures, depending on how much customization you need and how messy your existing data is. Timelines for a proper mortgage-specific setup usually run three to six months, sometimes longer if you're migrating years of borrower history from an old system. During that stretch, your team is often working in two systems at once, which is its own tax on productivity.

Then there's ongoing cost. Someone has to maintain the org: new fields when compliance requirements change, new automations when your process shifts, new user permissions when you hire. Larger shops keep a dedicated Salesforce admin on payroll and treat Salesforce CRM management as its own internal function, almost a program in its own right, for exactly this reason. Smaller brokerages usually can't justify that headcount, so they either let the system stagnate or keep paying the implementation partner for every small change.

None of this makes Salesforce a bad product. It makes it a big one. The question worth asking isn't "is Salesforce good," it's "does a 12-person mortgage brokerage need the same infrastructure as a 3,000-person bank."

There's also a slower cost that never shows up on an invoice: opportunity cost. Every week a loan officer spends half-trained on a system that's still being configured is a week of slower follow-up and borrowers who feel the lag even if they can't name it. Mortgage cycles are already stretched thin by underwriting timelines and rate volatility. Layering a multi-month software transition on top of that, during a season when the team needs to move fast, is a real tradeoff, not a footnote in a sales deck.

Why Salesforce Breaks Down for Mortgage-Specific Workflows

The mismatch shows up in daily use, not in the sales demo.

Loan officers live in borrower conversations that move fast: a rate lock question at 9pm, a document request the next morning, a referral partner asking for a status update by lunch. A platform built for generic B2B sales pipelines has to be heavily rebuilt to feel native to that rhythm. Even after a solid implementation, a lot of mortgage teams on Salesforce report the same friction: too many clicks to log a call, dashboards built for sales managers instead of loan officers, and automation rules that need a developer to touch every time a compliance requirement shifts.

This is exactly why a category of mortgage CRM software exists that isn't built on Salesforce at all. Teams get tired of paying for a platform that was designed for insurance agencies and real estate brokers, then retrofitted for mortgage. The best mortgage CRM for a given team is usually the one that already understands 1003 forms, LOS syncing, and borrower stage logic on day one, not the one that needs an implementation partner to teach it those concepts.

Take a simple example: a borrower's file moves from "conditional approval" to "clear to close." In a mortgage-native system, that stage change can already trigger the right document requests, notify the referral partner, and update the closing timeline, because the platform was built knowing that's how a loan moves. In a generic Salesforce org, someone has to design that logic first, test it, and maintain it every time compliance or investor requirements shift the definition of that stage. It's not that Salesforce can't do it. It's that every piece of mortgage-specific logic has to be built rather than already existing.

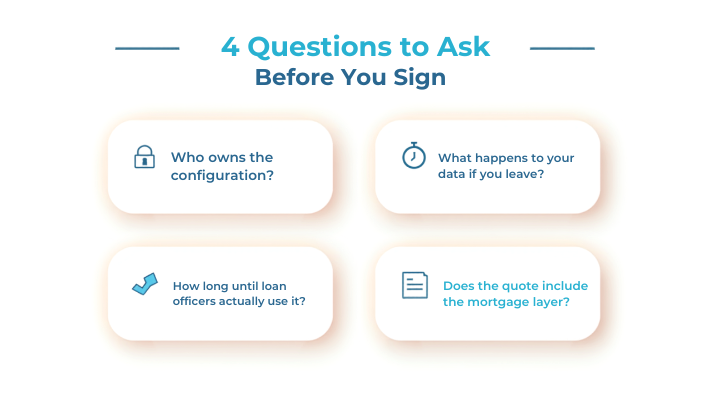

Questions to Ask Before You Sign With an Implementation Partner

A few questions save a lot of regret six months in:

Who owns the configuration once the project ends? If only the implementation partner understands the setup, you're locked into paying them for every change, and your Salesforce CRM program never really becomes yours.

What happens to your data if you leave? Salesforce orgs can be messy to export cleanly, especially after heavy customization.

How long until loan officers are actually working in the new system daily, not just logging in for training? Adoption lag is where a lot of the promised ROI quietly disappears.

Does the quote include the mortgage-specific layer, or just the base Salesforce implementation? These are often sold and priced separately, and it's easy to underestimate the second number.

Where MoserBus Fits Into the Picture

MoserBus was built for the opposite starting point. Instead of taking a general CRM and bolting mortgage logic onto it, the platform is mortgage-native from the first login: 1003 handling, document workflows, borrower portals, and pipeline stages that already match how loan officers actually work, not how a sales team works.

That matters most for the two things Salesforce implementations struggle with. First, time to value. There's no months-long configuration project standing between signing up and a loan officer actually using the system for a real borrower file. Second, cost structure. There's no separate implementation partner invoice sitting on top of the license, because the mortgage workflows are already there.

For brokerages and lending teams that don't have the headcount or budget for a dedicated Salesforce admin, that difference isn't cosmetic. It's the difference between a CRM that gets used every day and one that becomes a compliance checkbox nobody logs into after the first quarter.

There's a trust angle here too, and it's worth naming directly. A loan officer who has to fight a clunky system to log a borrower call starts cutting corners, and cutting corners on documentation is exactly the kind of thing that turns into a compliance headache later. A system that fits the actual workflow gets used honestly, because it's not adding friction to an already busy day. That's a bigger driver of clean audit trails than any feature list.

That doesn't mean Salesforce is the wrong choice for every lender. A large institution with a dedicated IT team, deep integration needs across dozens of departments, and budget to match genuinely benefits from that flexibility. But most mortgage brokers and small to mid-size lending teams aren't that. They need a system that works for a loan officer on day one, not a platform that becomes fully useful after two quarters of configuration.

If you're weighing the two, it's worth seeing how MoserBus handles pipeline setup side by side with what a Salesforce build would take, before signing an implementation contract you can't easily undo.

Frequently Asked Questions

Is Salesforce good for mortgage brokers? Salesforce can work for mortgage brokers, but it wasn't built for the industry out of the box. Most lenders need either a mortgage-specific layer like Jungo on top of it, or heavy custom configuration through an implementation partner, before it fits how loan officers actually work.

How much does a Salesforce implementation cost for a mortgage company? Costs vary widely based on team size and customization needs, but a proper mortgage-specific Salesforce Financial Services Cloud build with an implementation partner commonly runs from the low tens of thousands into six figures, plus ongoing admin costs.

What's the difference between Salesforce and a purpose-built mortgage CRM? Salesforce is a general CRM platform that needs configuration to handle mortgage-specific workflows like 1003 forms and LOS syncing. A purpose-built mortgage CRM like MoserBus already has those workflows in place, which usually means a shorter setup process and no separate implementation partner fee.

Do small mortgage brokerages need Salesforce? Usually not. Salesforce implementations make more sense for large lenders with dedicated IT resources and complex cross-department needs. Smaller brokerages and independent loan officers are typically better served by mortgage-native CRM software that doesn't require ongoing admin overhead.

If your team is closer to the second answer than the first, book a MoserBus demo and see what the platform looks like running a real pipeline before you spend a quarter deciding between Salesforce implementation partners.